Updated on October 5, 2024

Introduction

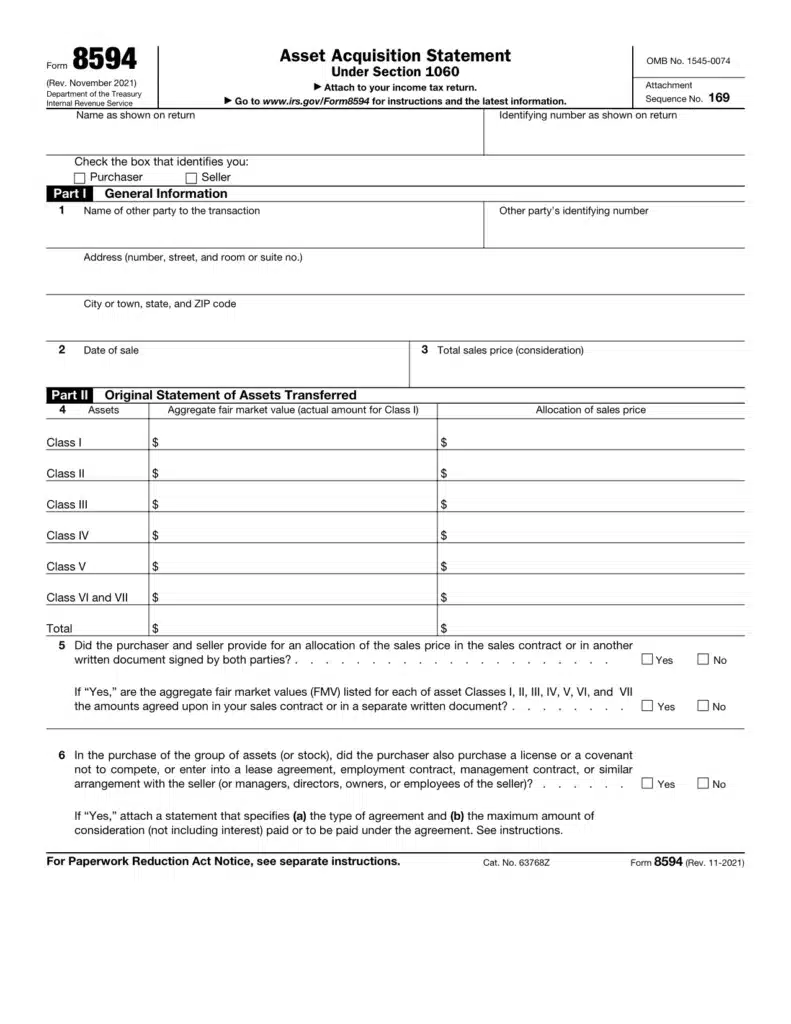

When acquiring a new business or a portfolio of assets, one crucial document stands between you and a seamless transaction: Form 8594. This IRS form, also known as the Asset Acquisition Statement, is essential for accurately reporting the allocation of purchase prices among various asset classes. Properly completing Form 8594 not only ensures compliance with tax regulations but also optimizes your tax obligations.

Key Requirements for Form 8594

- Filing Parties: Both the buyer and seller must attach Form 8594 to their respective income tax returns for the year in which the sale occurs.

- Asset Classes: The purchase price must be allocated among seven asset classes as defined by the IRS.

- Allocation Importance: Proper allocation affects the tax basis for each asset, influencing future depreciation deductions and capital gains calculations.

What is Form 8594 – Asset Acquisition Statement?

Form 8594 is a mandatory IRS document required when a group of assets constituting a trade or business is transferred. Both the buyer and seller must file this form to ensure the correct allocation of the purchase price across various asset classes.

This allocation directly impacts the tax obligations of both parties, affecting depreciation deductions for buyers and capital gains taxes for sellers.

Understanding the Seven Asset Classes

Accurately categorizing assets is crucial for completing Form 8594. Here are the seven asset classes defined by the IRS:

Class I: Cash and General Deposit Accounts

This includes cash, savings, and checking accounts held in banks or other depository institutions. Note that certificates of deposit are excluded from this class.

Class II: Actively Traded Personal Property & Certificates of Deposit

Includes actively traded personal property such as stocks, bonds, U.S. government securities, foreign currency, and certificates of deposit. Excludes stock of the seller’s affiliates.

Class III: Debt Instruments

Comprises accounts receivable and other debt instruments that are marked to market at least annually.

Class IV: Inventory

Includes property that would be part of the taxpayer’s inventory at the end of the tax year, stock in trade, and goods held primarily for sale to customers in the ordinary course of business.

Class V: Furniture, Fixtures, Vehicles, Land, and Equipment

Encompasses tangible assets such as buildings, furniture, fixtures, vehicles, and equipment that do not fall under other classes.

Class VI: Section 197 Intangibles

Includes intangible assets like workforce in place, client lists, business records, operating systems, databases, methods, designs, patterns, know-how, and formulas. Excludes goodwill and going concern value.

Class VII: Goodwill and Going Concern Value

Represents the excess of the purchase price over the fair market value of other assets acquired, including goodwill associated with a company’s reputation, branding, customer perception, and overall standing.

How to Fill Out Form 8594

Original Statement vs. Supplemental Statement

Understanding the difference between an original and a supplemental statement is key to correctly completing Form 8594.

Original Statement

- Complete Parts I and II.

- Include accurate identifying information such as names and Taxpayer Identification Numbers (TIN).

- Indicate your role as purchaser or seller by checking the appropriate box.

Supplemental Statement

- Complete Parts I and III.

- Use this when there is a reallocation in consideration after the original filing.

- Ensure all changes in asset allocation are accurately reflected.

Key Takeaways:

- Original statements require Parts I and II, while supplemental statements need Parts I and III.

- Always verify the accuracy of the information provided, including your TIN and role in the transaction.

Understanding Fair Market Value

Fair market value is critical when completing Form 8594. It represents the price an asset would sell for on the open market when both the buyer and seller are knowledgeable and not under pressure to transact.

When filling out Form 8594, fair market value determines the gross value of assets transferred, reduced by any mortgages, liens, pledges, or other liabilities associated with the assets.

Ensuring accurate fair market value helps prevent discrepancies that could lead to IRS audits or penalties.

Do You Need to File Form 8594?

If you’re acquiring a group of assets that constitute a trade or business, you must file Form 8594. This requirement applies whether the assets are held as a trade or business by both the seller and buyer.

Both parties must attach Form 8594 to their respective income tax returns, including individual returns (Forms 1040, 1041), partnership returns (Form 1065), and corporation returns (Forms 1120, 1120S).

If goodwill or going concern value is attached to the assets or could potentially attach, Form 8594 must be used to report the sale.

Failure to file Form 8594 when required can result in significant penalties—up to $50,000—and may lead to discrepancies that could trigger IRS audits.

The Importance of Accuracy on Form 8594 During Tax Season

Ensuring that Form 8594 is filled out accurately is essential for both buyers and sellers during tax season because it directly impacts how the transaction is reported to the IRS. Precision in this form helps you:

- Maintain Consistency: Both parties need to align on how they’re reporting the asset allocation. This prevents discrepancies that could lead to IRS audits or legal complications.

- Correctly Determine Tax Obligations: Accurate information allows sellers to properly calculate capital gains taxes, while buyers can correctly determine their depreciation deductions. Misreporting could result in overpaying taxes or attracting penalties.

- Ensure Compliance: The IRS mandates that the information on Form 8594 should match the entries on the annual tax returns of both parties. Consistent records safeguard against potential red flags that could trigger further scrutiny.

- Facilitate Smooth Transactions: Providing accurate details ensures that the closing process of the sale is seamless and supports a straightforward post-transaction relationship between the involved parties.

Consider using the expertise of tax professionals to navigate the complexity of Form 8594, ensuring all entries are precise and compliant with IRS requirements. This investment in accuracy not only protects you from potential penalties but also maximizes your financial outcomes.

How Asset Allocation Affects Taxes for Buyers and Sellers

When a business changes hands, the way assets are allocated plays a crucial role in determining the tax implications for both parties involved. Here’s how it affects buyers and sellers:

- Detailed Reporting Requirements: Both the buyer and the seller must meticulously report the transaction details using specific tax forms like Form 8594, which lists seven distinct asset categories integral to the process.

- Impact on Tax Liability: The classification of each asset can significantly affect tax liabilities. For buyers, some assets may offer depreciation benefits, allowing them to reduce taxable income over time. For sellers, the categorization can influence capital gains tax rates.

- Allocation Negotiations: Since the tax impact hinges heavily on asset allocation, negotiating how to distribute these assets in the sales agreement is critical. It’s not just about the sale price but also how the price is divided among various asset classes.

- Consistency Requirement: To avoid discrepancies, the IRS mandates that both parties apply a consistent approach to asset reporting. This means that the way assets are categorized and valued in the transaction must align on both the buyer’s and seller’s forms when filed as part of their annual tax returns.

By understanding and navigating these allocation intricacies, both buyers and sellers can strategically manage their tax outcomes, making it an essential part of the sales negotiation process.

The Importance of Reporting Business Asset Acquisitions in Detail

When you’re involved in acquiring a business, it’s crucial to meticulously report every asset involved. These assets can vary widely, encompassing both physical items and intangible elements. Accurate reporting plays a significant role in the transaction for several reasons:

- Impact on Taxes: The way assets are categorized greatly influences the tax responsibilities for both the buyer and the seller. The IRS recognizes seven distinct asset classes, each with different tax implications. Proper classification can affect depreciation schedules, tax credits, and deductions, ensuring both parties maximize their tax efficiency.

- Consistency in Reporting: It’s essential for the buyer and seller to use a consistent approach when handling the allocation of these assets. The IRS mandates that both parties report the transaction details in a uniform manner, as discrepancies can trigger audits or penalties. This consistency must be reflected in forms filed annually with tax returns, such as the Form 8594.

- Clarity in Negotiations: Including allocation discussions in the sales agreement provides clarity and reduces potential conflict. Negotiating asset allocation ahead of time ensures that both parties agree on the value and classification of each asset, streamlining the sales process and fostering transparency.

In summary, detailed reporting of business asset acquisitions not only optimizes tax outcomes but also maintains compliance with IRS regulations and supports smooth, conflict-free transactions.

Frequently Asked Questions (FAQ)

1. Why is it crucial to provide accurate information on Form 8594 during tax season?

Ensuring that Form 8594 is filled out accurately is essential for both buyers and sellers during tax season because it directly impacts the way the transaction is reported to the IRS. Precision in this form helps you:

- Maintain Consistency: Both parties need to align on how they’re reporting the asset allocation. This prevents discrepancies that could lead to IRS audits or legal complications.

- Correctly Determine Tax Obligations: Accurate information allows sellers to properly calculate capital gains taxes, while buyers can correctly determine their depreciation deductions. Misreporting could result in overpaying taxes or attracting penalties.

- Ensure Compliance: The IRS mandates that the information on Form 8594 should match the entries on the annual tax returns of both parties. Consistent records safeguard against potential red flags that could trigger further scrutiny.

- Facilitate Smooth Transactions: Providing accurate details ensures that the closing process of the sale is seamless and supports a straightforward post-transaction relationship between the involved parties.

Consider using the expertise of tax professionals to navigate the complexity of Form 8594, ensuring all entries are precise and compliant with IRS requirements. This investment in accuracy not only protects you from potential penalties but also maximizes your financial outcomes.

2. How does the allocation of assets affect taxes for buyers and sellers?

When a business changes hands, the way assets are allocated plays a crucial role in determining the tax implications for both parties involved. Here’s how it affects buyers and sellers:

- Detailed Reporting Requirements: Both the buyer and the seller must meticulously report the transaction details using specific tax forms like Form 8594, which lists seven distinct asset categories integral to the process.

- Impact on Tax Liability: The classification of each asset can significantly affect tax liabilities. For buyers, some assets may offer depreciation benefits, allowing them to reduce taxable income over time. For sellers, the categorization can influence capital gains tax rates.

- Allocation Negotiations: Since the tax impact hinges heavily on asset allocation, negotiating how to distribute these assets in the sales agreement is critical. It’s not just about the sale price but also how the price is divided among various asset classes.

- Consistency Requirement: To avoid discrepancies, the IRS mandates that both parties apply a consistent approach to asset reporting. This means that the way assets are categorized and valued in the transaction must align on both the buyer’s and seller’s forms when filed as part of their annual tax returns.

By understanding and navigating these allocation intricacies, both buyers and sellers can strategically manage their tax outcomes, making it an essential part of the sales negotiation process.

3. Why is it important to report business asset acquisitions in detail?

When you’re involved in acquiring a business, it’s crucial to meticulously report every asset involved. These assets can vary widely, encompassing both physical items and intangible elements. Accurate reporting plays a significant role in the transaction for several reasons:

- Impact on Taxes: The way assets are categorized greatly influences the tax responsibilities for both the buyer and the seller. The IRS recognizes seven distinct asset classes, each with different tax implications. Proper classification can affect depreciation schedules, tax credits, and deductions, ensuring both parties maximize their tax efficiency.

- Consistency in Reporting: It’s essential for the buyer and seller to use a consistent approach when handling the allocation of these assets. The IRS mandates that both parties report the transaction details in a uniform manner, as discrepancies can trigger audits or penalties. This consistency must be reflected in forms filed annually with tax returns, such as the Form 8594.

- Clarity in Negotiations: Including allocation discussions in the sales agreement provides clarity and reduces potential conflict. Negotiating asset allocation ahead of time ensures that both parties agree on the value and classification of each asset, streamlining the sales process and fostering transparency.

In summary, detailed reporting of business asset acquisitions not only optimizes tax outcomes but also maintains compliance with IRS regulations and supports smooth, conflict-free transactions.

4. How do you fill out Form 8594 for an original statement versus a supplemental statement?

Understanding the difference between an original and a supplemental statement is key to correctly completing Form 8594.

Original Statement

- Parts to Complete: Fill Parts I and II.

- Details Required: Include accurate identifying information such as names and Taxpayer Identification Numbers (TIN).

- Designation: Indicate whether you are the purchaser or seller by checking the appropriate box.

Supplemental Statement

- Parts to Complete: Fill Parts I and III.

- When to Use: Apply this when there is a reallocation in consideration after the original filing.

- Accuracy: Ensure all changes in asset allocation are accurately reflected.

Key Takeaways:

- Original statements require Parts I and II, while supplemental statements need Parts I and III.

- Always verify the accuracy of the information provided, including your TIN and role in the transaction.

By following these guidelines, you’ll efficiently manage Form 8594, tailoring your submission to fit whether it’s original or supplemental.

Filing Deadlines

Form 8594 must be filed with the tax return for the year in which the sale occurs. If there are adjustments in consideration after that year, a new Form 8594 should be filed alongside the tax return for the year in which those changes are recognized.

Adhering to these deadlines is crucial to avoid penalties and ensure that your asset allocation is accurately reported.

Penalties for Non-Compliance

Failure to file Form 8594 when required can result in significant penalties—up to $50,000. Additionally, discrepancies between reported allocations by buyer and seller can lead the IRS to disregard your reported allocations and impose their own, which could be less favorable.

Ensuring accurate and timely filing of Form 8594 helps avoid these penalties and maintains compliance with IRS regulations.

In Conclusion

IRS Form 8594 is essential for accurately allocating the purchase price among different asset categories in a business acquisition. Both the seller and buyer must file this form and attach it to their income tax returns to ensure compliance with IRS regulations.

Proper allocation impacts tax bases, depreciation deductions, and capital gains calculations, making accuracy paramount. Utilizing tax professionals can help navigate the complexities of Form 8594, ensuring precise and compliant entries.

By understanding the requirements and meticulously completing Form 8594, you can streamline your asset acquisition process, optimize your tax outcomes, and avoid potential IRS complications.

Need Help with Tax Form 8594?

Do you need assistance with filing Tax Form 8594 for your business acquisition? Our expert team is here to help!

Filing Form 8594 can be complex and time-consuming. Mistakes can lead to penalties and legal issues. Let our experienced professionals guide you through the process, ensuring accurate allocation of purchase prices and compliance with IRS requirements.

Don’t let the complexities of Form 8594 hold you back from a successful acquisition. Contact us today and let us help you navigate the process for a smooth and compliant business transaction.

>> You may find this interesting: What Happens If You Get Audited And Don’t Have Receipts?

anywhere

anywhere  anytime

anytime