Understanding how to calculate gross income is a fundamental skill for both individuals and businesses. It forms the basis for financial assessments, tax computations, and effective budgeting. In this comprehensive guide, we’ll walk you through the essential concepts and instructions to accurately determine your gross income, whether you’re a salaried employee, a business owner, or simply seeking to gain a deeper understanding of your financial situation.

Key Takeaways

- Gross income for an individual includes income from wages and salary together with other forms of income, including pensions, interest, dividends, and rental income.

- Gross income for a business is total revenues minus the cost of goods sold.

- Individual gross income is part of an income tax return and—after certain deductions and exemptions—becomes adjusted gross income, then taxable income.

- Businesses often use gross income instead of net income to better gauge the product-specific performance of the business.

What is Gross Income?

For individuals, gross income is often referred to as gross pay on paychecks, representing an individual’s total earnings before paying for taxes and other deductions. It encompasses all sources of income, extending beyond cash, and covers property or services received.

In the business context, gross income is synonymous with terms like gross margin or gross profit. A company’s gross income, as seen on the income statement, is the revenue from all sources minus the cost of goods sold (COGS).

The Importance of Gross Income

Understanding your gross income is crucial because it serves various purposes that can significantly impact your financial situation, including:

- Rental Housing: Landlords assess applicants’ gross income to gauge their ability to pay rent.

- Loan Approval: Lenders use gross income to determine loan eligibility.

- Tax Calculation: Tax agencies rely on gross income to calculate taxes owed.

- Salary Negotiations: Applicants can use their gross income as a basis for salary discussions.

- Credit Limit: Credit issuers evaluate gross income to establish credit limits.

How to Calculate Your Total Gross Income

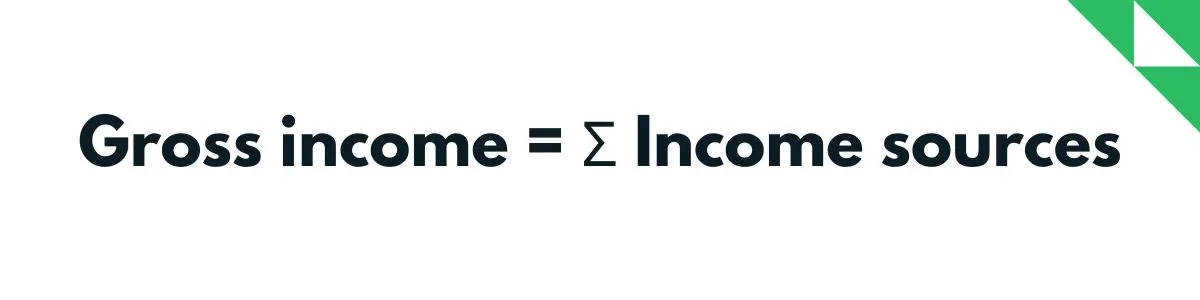

To calculate your gross income in total, sum up all your income sources before any deductions or taxes are taken out. It should include:

- Regular salary

- Bonuses

- Commissions

- Earnings from side jobs

- Freelance income

- Extra income

- Supplemental Security Income (SSI)

- Dividend payments

- Interest

- Capital gains

The formula for gross income is:

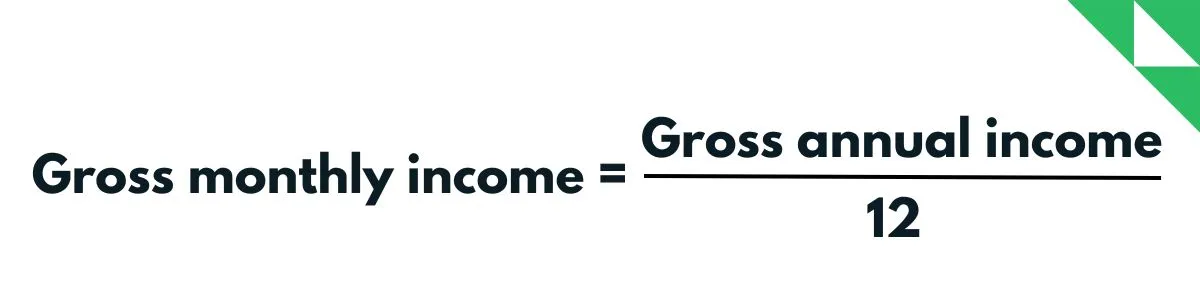

Calculate Monthly Gross Income for Individuals

If you wonder how to calculate your gross monthly income, here’s the process of determining gross income based on the nature of an individual’s income sources:

Salaried Worker

To calculate gross income, simply divide the annual salary by 12 to derive the monthly gross income figure.

Hourly Worker

To calculate your gross monthly income when you’re paid hourly, use this formula:

| Gross monthly income = (Hourly pay x Hours worked per week x 52) / 12 |

Here are the steps for calculating your gross monthly income as an hourly or salaried employee:

- Begin by listing all your income sources, such as from pay stubs or other records. Make sure to include each income source only once, and consider listing them vertically to make adding the figures easier.

- Convert your annual income into a monthly value. If you’re paid hourly, first determine your weekly income by multiplying your hourly pay by the number of hours worked per week (e.g., $15/hour x 40 hours/week = $600/week). Then, multiply your weekly income by the number of weeks you work in a year (e.g., $600/week x 52 weeks = $31,200/year). Finally, divide your annual income by 12 to account for the number of months in a year:

You can also use a computer program with an automated formula to enhance the accuracy of your calculations. Regardless of the method you choose, it’s essential to double-check your results for precision. Including all decimal values instead of rounding can further enhance the accuracy of your calculations.

Calculate Monthly Gross Income for Businesses

The formula for finding gross annual income for a business is subtracting the cost of goods sold from the gross revenue. Follow the step-by-step guidelines below:

- Identify the company’s yearly revenue by checking records or seeking input from management or financial experts who can access this information quickly.

- Determine the cost of sales, which may involve services provided or goods sold, and subtract it from the annual revenue. Collaborate with auditors, accounting professionals, and relevant departments to gather accurate figures. This subtraction yields the company’s gross annual income.

- Convert the gross annual income into a monthly value by dividing it by 12, giving the average monthly gross income using the equation:

| Gross monthly income = Gross annual income / 12 |

Gross Income vs Net Income: What’s the Difference?

Gross income and net income are terms often used by businesses to indicate profit. They are also relevant when discussing a household’s earnings.

For an individual, net income is the total amount of money earned after subtracting all the taxes and deductions applicable from the gross income. An individual’s net income aligns closely with their final paycheck; although the paycheck doesn’t cover all expenses, it’s a clear illustration of revenue reduced by costs.

| Net Income = Gross Income – Taxes – Other deductions (garnishment, health insurance, retirement plan, job-related expenses, etc.) |

For a business, net income is the total amount of revenue minus all the costs. These expenses include the cost of goods sold just like gross income. However, net income also takes into account the selling, general, administrative, tax, interest, and other expenses that are not included in the calculation of gross income.

What is Adjusted Gross Income (AGI)?

Adjusted Gross Income (AGI) is the amount you get after subtracting specific deductions from your total income. These deductions include things like contributions to retirement accounts or student loan interest. AGI is a crucial starting point for figuring out your taxable income, which is the amount of your income that is subject to taxes. It’s also important for determining your eligibility for certain tax credits and deductions. When you e-file your taxes, your previous year’s AGI is used as a verification measure.

What is Modified Adjusted Gross Income (MAGI)?

Modified Adjusted Gross Income (MAGI) builds on AGI by making additional adjustments based on specific tax benefits and contributions you might be eligible for. It’s a flexible calculation tailored to your financial situation. MAGI helps determine your eligibility for things like tax deductions, credits, and contributions to accounts like health savings accounts (HSAs) and retirement plans. Essentially, MAGI refines the AGI calculation to fit individual financial scenarios and ensure accurate tax benefits.

Conclusion

In conclusion, knowing how to calculate gross income empowers individuals to budget effectively, businesses to assess their revenue streams, and everyone to grasp the essentials of financial planning. It’s a concept that unlocks a deeper understanding of economic well-being and helps guide smart financial decisions.

FAQ

Why is Gross Income Important for Tax Purposes?

Gross income is crucial for tax purposes because it serves as the starting point for determining how much of your income is subject to taxation. When you file your taxes, you start with your gross income and then apply various deductions and exemptions to arrive at your taxable income. This process helps determine the amount of income on which you owe taxes to federal and state governments. Understanding your gross income is essential for accurate tax calculations, eligibility for specific tax credits, and compliance with tax laws.

Do Self-Employed Individuals Calculate Gross Pay Differently?

Yes, self-employed individuals typically calculate gross income differently than traditional employees. For employees, gross income is usually the total amount earned before taxes and deductions. However, self-employed individuals must account for both their business income and the business expenses associated with generating that income. Their gross income is determined by subtracting business expenses from their total business revenue. This approach ensures that the income is calculated based on the actual profit the business generates, rather than the gross revenue alone.

Are Bonuses Included in Gross Income?

Yes, bonuses are generally included in gross income. Bonuses, like regular salary or wages, are a form of compensation received for work performed, and they contribute to an individual’s overall earnings. When calculating gross income for tax purposes, bonuses are added to the total income from all sources, which includes salary, hourly wages, rental income, dividends, and other forms of earned income. The total gross income serves as the starting point for tax calculations, determining taxable income, and eligibility for tax benefits.

How do you calculate annual gross income in four steps?

How to Calculate Your Annual Gross Income in Four Simple Steps

Understanding your annual gross income is crucial for both personal budgeting and meeting tax obligations. Here’s a straightforward guide to help you accurately determine this figure.

- Start with Your SalaryYour primary source of earnings is typically your salary. Depending on how you are paid, the calculation varies:

- Hourly Wage: Multiply your hourly rate by the total hours worked in a year (usually 2,080 for full-time positions).

- Monthly Salary: Simply multiply by 12 to get the annual total.

- Consider Additional Income StreamsBeyond your regular salary, you might have other revenue sources. Include:

- Bonuses: If you receive bonuses (e.g., $1,000 quarterly), add that up for the year.

- Side Jobs or Freelance Work: Calculate any extra earnings from part-time gigs.

- Investment Income: Don’t forget dividends or interest from investments.

Every source counts, so be sure to capture all possible income that contributes to your financial picture.

- Account for Qualified DeductionsSome deductions can decrease your gross income for tax purposes:

- Retirement Contributions: Payments into 401(k) or IRA are often deductible.

- Health Savings Accounts (HSA): Similar to retirement accounts, these are also typically deductible.

Subtract these from the total calculated in the previous steps to get closer to the final amount.

- Sum Up for the Annual TotalNow, bring all components together. Combine your base salary and additional income sources, then subtract deductions. This final sum is your annual gross income, reflecting an accurate picture of your yearly earnings.

By following these steps, you’ll arrive at a precise calculation of your annual financial standing, ensuring you have the information needed for effective planning and compliance.

How do you calculate annual gross income from a biweekly paycheck?

How to Calculate Annual Gross Income from a Biweekly Paycheck

If you receive payments every two weeks, determining your annual gross income is straightforward. Here’s how you can do it:

- Identify Your Biweekly Paycheck Amount:Check your most recent pay stub for the total amount before deductions. This figure is your biweekly gross pay.

- Calculate the Annual Total:Since there are 26 two-week periods in a year, multiply your biweekly gross pay by 26.

Here’s the formula for clarity:

Annual Gross Income = Biweekly Pay × 26

Using this method gives you a clear picture of your yearly earnings before any taxes or other deductions are applied.

What are the key components of annual gross income?

Understanding Annual Gross Income

Annual gross income is a crucial figure in your financial landscape, representing the total earnings before any deductions or taxes. Let’s explore what constitutes this comprehensive income measure.

What Counts as Annual Gross Income?

It’s important to know exactly what to include when calculating your annual gross income. Here are the primary components:

- Wages and Salaries: Your base income from employment, as specified in your employment contract, is usually paid on a regular schedule such as weekly or monthly.

- Tips and Bonuses: Additional earnings include tips, common in service industries, and bonuses, often tied to performance metrics or milestones achieved.

- Self-employment Income: If you’re running a business or freelancing, your income from these activities is part of your gross income, though business expenses can mitigate taxable amounts.

- Rental Income: Money received from renting out property is another component, including earnings from both real estate and personal rentals.

- Investment Income: Returns from investments—like dividends, interest, and profits from selling stocks—contribute to your gross income.

- Alimony Received: Court-ordered financial support from an ex-spouse is taxable and should be counted in your gross income.

- Social Security Benefits: Depending on your other income, a portion of Social Security benefits may be taxable and included in your gross income.

- Miscellaneous Income: This includes any other earnings not categorized above, such as royalties, prizes, or income from selling personal items.

By understanding these components, you can ensure a thorough and accurate calculation of your annual gross income, setting a solid foundation for financial planning and tax preparation.

What are some useful tips when calculating annual gross income?

Essential Tips for Calculating Your Annual Gross Income

Calculating your annual gross income accurately is crucial for managing your finances effectively. Here are some tips to streamline the process and ensure precision.

- Leverage Technology Tools: There’s a wealth of digital tools available to help demystify financial calculations. Utilize online calculators or personal finance applications to automate and verify your income figures. These platforms often include specialized features to assist with income tracking and deduction assessments.

- Consult Financial Experts: If navigating the complexities of income calculations feels overwhelming, consider reaching out to a tax advisor or financial planner. These professionals can provide insights and guidance, particularly if your finances involve intricate deductions or multiple income streams.

- Keep Detailed Records: Maintaining thorough records of all your earnings and deductions is foundational for accurate income calculation. Organize your pay stubs, investment statements, and other financial documents. This practice ensures you have everything you need for precise calculations and simplifies tax preparation.

- Regular Financial Reviews: Income levels may vary, especially with investments or side jobs. Regularly review your financial statements to stay informed about your earnings. This will help you adjust your calculations and avoid unexpected discrepancies at year’s end.

- Stay Updated on Tax Changes: Tax laws and deductions are subject to change. Keeping informed about the latest tax codes and understanding applicable deductions will help you calculate your gross income more accurately. Being proactive in this area is essential for reliable financial planning.

Does annual gross income affect your credit score?

Does Annual Gross Income Affect Your Credit Score?

Many people wonder if their annual gross income plays a role in determining their credit score. Simply put, your income doesn’t directly influence your credit score. However, it can still play an important part in your overall financial profile.

How Lenders Use Income

While the credit score itself is calculated based on factors like payment history, credit utilization, and length of credit history, lenders often look at your income as well. Here’s why:

- Debt-to-Income Ratio: Lenders assess your ability to repay by looking at the ratio of your monthly debt payments to your gross income. A lower ratio is usually preferable.

- Creditworthiness: High earnings can demonstrate a stronger borrowing capacity, which might make lenders more willing to approve loans or offer better terms.

Credit Score Components

To understand how your score is calculated, consider these key elements:

- Payment History: Consistently paying bills on time has the largest impact.

- Credit Utilization: It’s the percentage of available credit you’re using. Lower usage can positively affect your score.

- Length of Credit History: Longer credit histories tend to benefit your score.

- New Credit and Credit Mix: Managing different types of credit accounts responsibly can also enhance your score.

In summary, while your annual gross income itself doesn’t impact your credit score, it remains a critical aspect when lenders evaluate your financial health. Knowing how income fits into the broader picture can help you better prepare when applying for credit.

What income sources are excluded from annual gross income?

What Income Sources Are Excluded from Annual Gross Income?

Understanding which income sources aren’t part of your taxable income is crucial for accurately reporting your finances. Here’s a rundown of income exclusions that can impact your taxable amount:

- Gifts and Inheritances: Money or property received as gifts or through inheritance is typically not treated as taxable income. While taxes might apply to the donor or the estate, recipients usually don’t include these funds in their annual gross income.

- Life Insurance Payouts: If you’re a beneficiary of a life insurance policy, the money you receive following the policyholder’s passing is generally not taxable. Be aware of exceptions, such as any interest earned or if you acquired the policy in exchange for payment.

- Child Support: Money received for child support is not considered taxable income. This ensures that funds intended for a child’s well-being aren’t taxed, distinguishing them from alimony, which may be taxable.

- Workers’ Compensation: Compensation benefits received due to workplace injuries are excluded from gross income. This allows individuals to focus on recovery without the burden of additional taxes on these benefits.

- Scholarships and Fellowships: Financial aid for educational purposes, such as scholarships or fellowships, is often excluded if used for tuition, mandatory fees, books, or supplies. However, funds used for accommodation or meals might still be taxable.

By recognizing these exclusions, you can better manage your financial reports and avoid overstating your taxable income.

Where can you find your gross annual income on a tax return?

Finding your gross annual income on a tax return is straightforward and typically located on the very first page of the document. Look for it labeled as “Total Income” or “Gross Income.”

The specific line number where this appears may vary based on the tax form you are using and the tax year in question. Here’s how you can locate it:

- Identify the Form: Different forms like 1040, 1040A, or 1040EZ will have variations in line numbers.

- Check the Year: Tax laws and forms can change annually, so ensure you’re looking at the right year’s form.

- Consult the Instructions: Each tax form comes with detailed instructions that can direct you to the correct line.

If in doubt, compare with previous returns or consult with a tax professional. This ensures you accurately identify your gross annual income without hassle.

When should you seek professional help for calculating income?

When to Seek Professional Help for Calculating Income

Navigating the world of personal finance can often feel overwhelming, especially when it comes to calculating income accurately. Here’s when you should consider seeking guidance from a tax professional or financial planner:

- Complex Financial Situations: If your financial picture includes multiple income streams, investments, or business activities, professional insight can help you make sense of it all.

- Changing Financial Circumstances: Major life changes such as marriage, divorce, or starting a business can significantly impact your finances. An expert can guide you through these transitions smoothly.

- Uncertainty About Tax Deductions and Credits: When you’re unsure about which deductions or credits apply to you, seeking a pro can ensure you’re taking full advantage of what’s available.

- Preparing for Tax Season: To maximize your tax refund or minimize your liability, consulting a professional can be invaluable. They’ll help you avoid mistakes that could lead to audits or penalties.

- Future Financial Planning: If you’re planning for the future, whether it’s saving for retirement or buying a home, a financial planner can help you strategize effectively.

These experts can provide tailored advice, ensuring your calculations are precise and your financial decisions are well-informed.

Why is it important to maintain accurate records and documentation?

Why Maintaining Accurate Records and Documentation is Crucial

Proper record-keeping is essential for a myriad of reasons. At the heart of financial management is the need to ensure that all earnings and deductions are meticulously tracked. This involves consistently updating and filing away pay stubs, investment records, and other pertinent financial documents.

Benefits of Accurate Records

- Facilitates Accurate Income Calculation: By maintaining detailed documents, you ensure that every aspect of your financial picture is clear and correct. This accuracy is vital not only for current expenses but for long-term financial planning as well.

- Streamlines the Tax Process: When tax season rolls around, having organized documentation makes filing returns less stressful and more efficient. You’ll have all necessary information at your fingertips, reducing the risk of errors or omissions that could lead to penalties.

- Essential for Audits: In the event of a financial audit, comprehensive and precise records provide a layer of protection. They help to quickly verify your claims and maintain transparency with auditors.

- Supports Financial Decisions: With a clear financial overview, you can make more informed decisions about investments, cost-cutting, and growth opportunities. Sound documentation is a resource when discussing finances with advisors or potential business partners.

In essence, accurate record-keeping is not just a chore—it’s a fundamental practice that supports both your personal and professional financial health. Investing time in developing a robust organizational habit pays dividends in clarity and peace of mind.

How often should you review your financial statements?

How Often Should You Review Your Financial Statements?

To effectively manage your financial health, regularly reviewing your financial statements is crucial. But how often is “regularly”? Let’s break it down:

Monthly Check-ins

For fluctuating incomes from sources like investments or side gigs, monthly reviews are ideal. This frequency allows you to stay current with your earnings and spending patterns, helping you identify trends or discrepancies early on.

Quarterly Reviews

A quarterly review is beneficial for more significant financial decisions. It provides a more comprehensive overview, making it easier to adjust your financial strategies and targets for the coming months.

Annual Overview

At a minimum, perform an annual review of your financial statements. This is crucial for reflecting on the financial year as a whole and planning for the next. Understanding your annual income and expenses helps you set realistic goals and prepare for tax obligations.

By incorporating these regular reviews into your schedule, you can better manage your financial situation and avoid any unpleasant surprises when filing taxes or making significant life decisions.

anywhere

anywhere  anytime

anytime